Nepal just failed to exit the FATF grey list for the second review cycle in a row.

Most of the commentary on this treats it as a legal or diplomatic problem. It isn't, mostly. Four of FATF's six conditions for Nepal are fundamentally about visibility — knowing where the risk sits, watching transactions as they happen, tracing assets after the fact. That's a systems and data problem, and it has a different playbook than passing another law.

Every reform in the RSP Bacha Patra and Budget 2083/84 depends on the quality of the people running the institutions that implement them. This is not an abstract governance concern. It is the most concrete prerequisite for everything else working.

Nepal's budget reinstates Take or Pay PPAs. Silicon Himalayas

breaks down the six bankability requirements DFIs demand —

and where Nepal's PPA templates have historically fallen short.

Nepal's FITTA amendment is the most talked-about provision

in the FY 2083/84 budget. "Notification instead of NRB

approval for repatriation."

But what does that actually change — and what doesn't change

until NRB publishes implementing directives?

We've broken it down: the three-layer current framework,

what "notification sufficient" structurally changes for

PE/VC timing and hybrid instruments, and the four specific

risks to watch before restructuring your transaction documents.

Nepal's budget just committed to splitting NEA into three

separate companies — generation, transmission, and

distribution/trading.

For hydropower developers and project finance advisors,

this creates three new counterparties where one existed

before. Three new risk profiles. And a PPA sequencing

problem that no one is talking about yet.

NEA unbundling has been in Nepal's policy documents since

2008. What's different this time — and what the transition

architecture still needs to answer — is what our latest

brief covers.

"Will complete" in a budget speech is not the same as

"has completed."

Nepal's NPR 2,124 billion budget for FY 2083/84 is the most reform-coherent fiscal document in a decade. This institutional analysis cuts through the headline numbers to examine what the NEA unbundling, FITTA amendment, cross-border electricity trading, LLP framework, and capital market provisions actually mean for developers, fund managers, and institutional investors — and what to watch in the first 90 days.

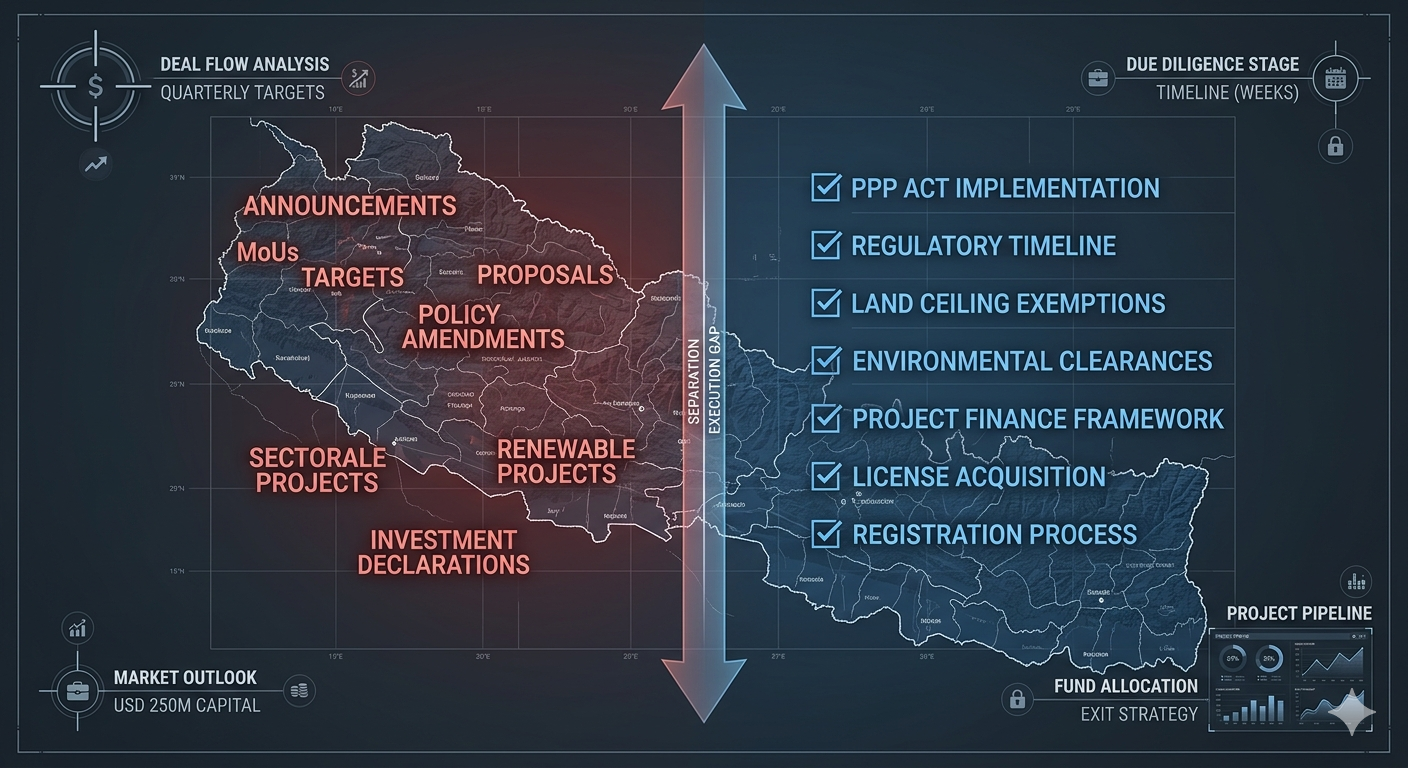

Nepal's investment gap is not primarily a capital problem. It is an infrastructure problem. Capital without institutional infrastructure doesn't flow — it walks away.